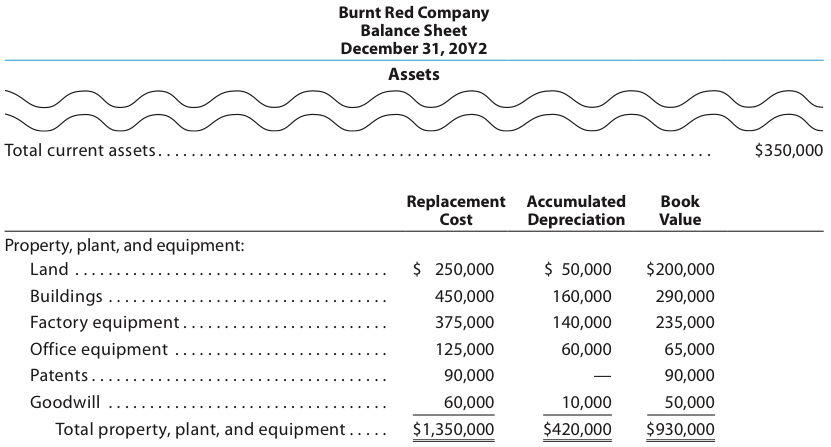

The following table shows the sales and average book value of fixed assets for three different companies from three different industries for a recent year:

Company (Industry) Sales (in millions) Average Book Value of Fixed Assets (in millions) Alphabet (Google) Inc. (Internet) $ 74,989 $ 26,450 Comcast Corporation (communications) 74,510 32,309 Wal-Mart Stores, Inc. (retail) 485,651 117,281

a. For each company, determine the fixed asset turnover ratio. Round to one decimal place.

b. Explain Comcast’s fixed asset turnover ratio relative to the other two companies.

Answer:

a.

Fixed Asset Turnover Ratio =

Comcast:

=Wal-Mart:

Alphabet (Google) Inc.:

$74,989

$26,450

$74,510

$32,309

$485,651

$117,281

2.8 2.3 4.1

Sales

Average Book Value of Fixed Assets

b. Comcast’s fixed asset turnover is less than the other two companies. This means

Comcast is less efficient at generating sales from fixed assets than the other two

companies. This can be explained by the nature of Comcast’s business. Comcast

must build a complete cable network in order to earn revenues. This includes

underground cable through cities, neighborhoods, and individual residences. In

addition, Comcast must provide the additional technology to carry broadband over

this network. As a result, Comcast has a significant investment in fixed assets in

order to earn revenues. Alphabet (Google) has a significant investment in servers;

however, these servers are able to generate advertising revenue more efficiently than

Comcast is able to earn subscription revenues over its cable network. Wal-Mart’s

major fixed assets are its stores. However, Wal-Mart’s other major asset is

merchandise inventory, which is not included in the fixed asset turnover ratio.

Thus, Wal-Mart’s higher asset efficiency is only partially explained by the fixed asset

turnover ratio. The inventory turnover ratio would also need to be analyzed to fully

appreciate Wal-Mart’s efficiency in using its total assets. The other two companies do

not have merchandise inventory, so the fixed asset turnover ratio is a more complete

measure of their total asset efficiency relative to Wal-Mart’s.