The beginning inventory for Dunne Co. and data on purchases and sales for a three-month period are shown in Problem 7-1B.

Instructions

1. Determine the inventory on June 30 and the cost of merchandise sold for the three-month period, using the first-in, first-out method and the periodic inventory system.

2. Determine the inventory on June 30 and the cost of merchandise sold for the three-month period, using the last-in, first-out method and the periodic inventory system.

3. Determine the inventory on June 30 and the cost of merchandise sold for the three-month period, using the weighted average cost method and the periodic inventory system. Round the weighted average unit cost to the dollar.

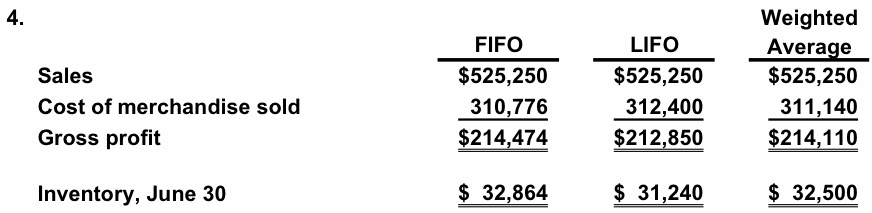

4. Compare the gross profit and June 30 inventories using the following column headings:

FIFO LIFO Weighted Average Sales Cost of merchandise sold Gross profit Inventory, June 30

Answer:

1. First-In, First-Out Method

Merchandise inventory, June 30................................................. $ 32,864

Cost of merchandise sold........................................................... 310,776

Supporting computations

Merchandise inventory:

26 units @ $1,264............................................................... $ 32,864

Cost of merchandise sold:

Beginning inventory, April 1....................................................... $ 30,000

Purchases............................................................................... 313,640

Merchandise available for sale.................................................... $343,640

Less ending inventory, June 30................................................... 32,864

Cost of merchandise sold......................................................... $310,776

2. Last-In, First-Out Method

Merchandise inventory, June 30................................................ $ 31,240

Cost of merchandise sold.......................................................... 312,400

Supporting computations

Merchandise inventory:

25 units @ $1,200............................................................... $30,000

1 unit @ $1,240............................................................... 1,240

26 units........................................................................... $31,240

Cost of merchandise sold:

Beginning inventory, April 1...................................................... $ 30,000

Purchases................................................................................. 313,640

Merchandise available for sale................................................... $343,640

Less ending inventory, June 30................................................. 31,240

Cost of merchandise sold.........................................................

3. Weighted Average Cost Method

Merchandise inventory, June 30.................................... $ 32,500

Cost of merchandise sold............................................. 311,140

Supporting computations

$343,640

275 units

Merchandise inventory:

26 units × $1,250 = $32,500

Cost of merchandise sold:

Beginning inventory, April 1....................................... $ 30,000

Purchases.................................................................. 313,640

Merchandise available for sale.................................... $343,640

Less ending inventory, June 30.................................... 32,500

Cost of merchandise sold............................................. $311,140

$312,400

4.Weighted

FIFO LIFO Average

Sales$525,250 $525,250 $525,250

Cost of merchandise sold 310,776 312,400 311,140

Gross profit $214,474 $212,850 $214,110

Inventory, June 30 $ 32,864 $ 31,240 $ 32,500

No comments:

Post a Comment