a. Determine the direct labor rate, direct labor time, and total direct labor cost variance for the (1) Cutting Department and (2) Sewing Department.

b. Interpret your results.

Answer:

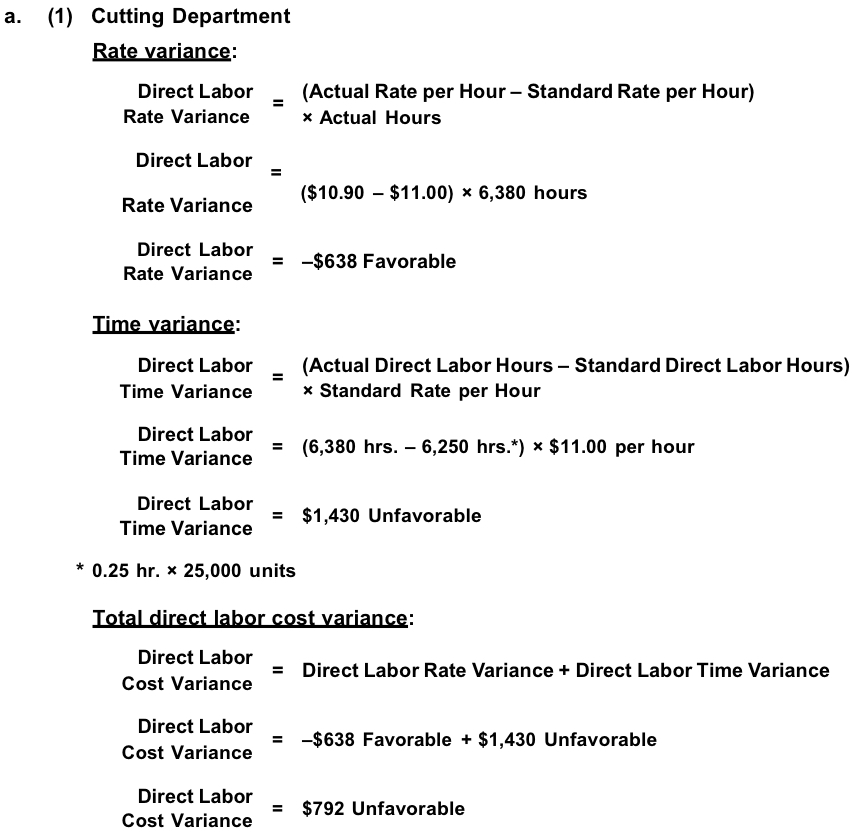

a. (1) Cutting Department

Rate variance:

Direct Labor

Rate Variance =

(Actual Rate per Hour – Standard Rate per Hour)

× Actual Hours

Direct Labor =

Rate Variance ($10.90 – $11.00) × 6,380 hours

Direct Labor

Rate Variance

Time variance:

Direct Labor

Time Variance

= –$638 Favorable

= (Actual Direct Labor Hours – Standard Direct Labor Hours)

× Standard Rate per Hour

Direct Labor

Time Variance

Direct Labor

Time Variance

= (6,380 hrs. – 6,250 hrs.*) × $11.00 per hour

= $1,430 Unfavorable

* 0.25 hr. × 25,000 units

Total direct labor cost variance:

Direct Labor

Cost Variance

Direct Labor

Cost Variance

= Direct Labor Rate Variance + Direct Labor Time Variance

= –$638 Favorable + $1,430 Unfavorable

Direct Labor

Cost Variance

= $792 Unfavorable

(2) Sewing Department

Rate variance:

Direct Labor

Rate Variance =

(Actual Rate per Hour – Standard Rate per Hour)

× Actual Hours

Direct Labor =

Rate Variance (

$11.12 – $11.00) × 9,875 hours

Direct Labor

Rate Variance

Time variance:

Direct Labor

Time Variance

= $1,185 Unfavorable

= (Actual Direct Labor Hours – Standard Direct Labor Hours)

× Standard Rate per Hour

Direct Labor

Time Variance

= (9,875 hrs. – 10,000 hrs.*) × $11.00 per hour

Direct Labor

Time Variance

= –$1,375 Favorable

* 0.40 hr. × 25,000 units

Total direct labor cost variance:

Direct Labor

Cost Variance =

Direct Labor Rate Variance + Direct Labor Time Variance

Direct Labor

Cost Variance

= $1,185 Unfavorable – $1,375 Favorable

Direct Labor

Cost Variance

= –$190 Favorable

b. The two departments have opposite results. The Cutting Department has a

favorable rate and an unfavorable time variance, resulting in a total unfavorable

cost variance of $792. In contrast, the Sewing Department has an unfavorable rate

variance, but has a favorable time variance, resulting in a total favorable cost

variance of $190. The causes of this disparity are worthy of investigation. There

are many possible causes including tight or loose standards, inferior or superior

operating methods, and inappropriate or appropriate use of overtime. Combining

both departments, the overall operation shows an unfavorable cost variance of $602

($792 – $190), as a result of the weak performance in the Cutting Department.

No comments:

Post a Comment