Answer:

GIOVANNI COMPANY

Income Statement Through Gross Profit

For the Year Ended December 31, 2014

Sales (3,500 units × $400) $1,400,000

Cost of goods sold—at standard* 1,093,750

Gross profit—at standard $ 306,250

F

avorable Unfavorable

Less variances from standard cost:

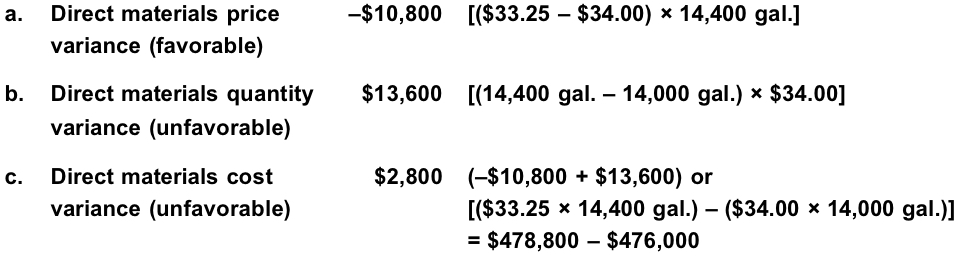

Direct materials price (PE23–1A) $10,800

Direct materials quantity (PE23–1A) $13,600

Direct labor rate (PE23–2A) 8,850

Direct labor time (PE23–2A) 6,000

Factory overhead controllable (PE23–3A) 2,150

Factory overhead volume (PE23–4A) 900 (18,900)

Gross profit $ 287,350

* Direct materials (3,500 units × 4 gal. × $34.00)……………………………………………………

$ 476,000

Direct labor (3,500 units × 5 hrs. × $30.00)……………………………………………………… 525,000

Factory overhead [3,500 units × 5 hrs. × ($3.50 + $1.80)]……………………………………… 92,750

Cost of goods sold at standard……………………………………………………………………… $1,093,750